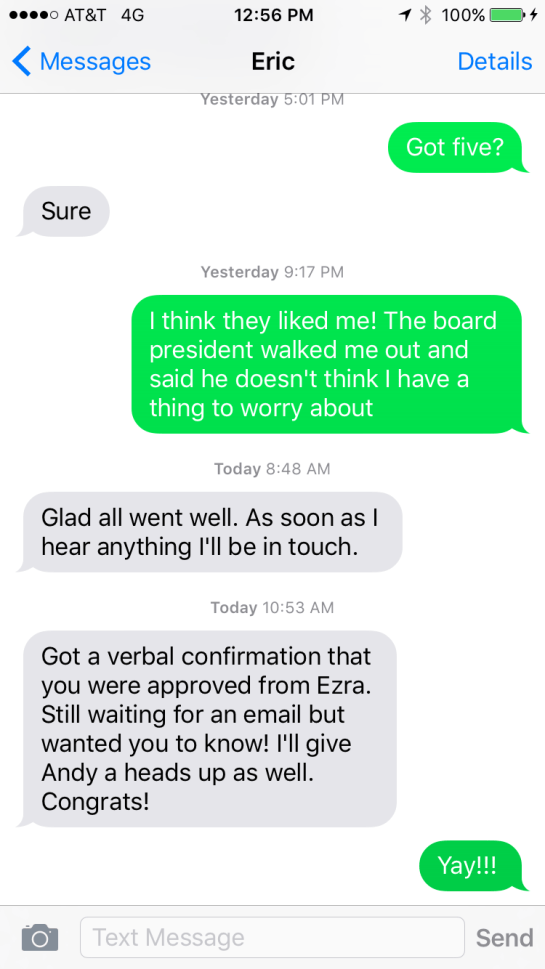

last week, when i first received the draft contract for the grand apartment, my lawyer sent a list of “key takeaways” (his assumption being, of course, that i wouldn’t read the entire contract myself. BUT I DID. not that i understood it, but i tried!). the list looked a little something like this (key areas removed for privacy’s sake):

- Purchaser – Sarah Jacobson

- Apartment – Apt X, Grand Street, New York, NY 10002

- Apartment to be vacant and in broom clean condition at time of closing with the standard items listed in 1.11. Anything else they told you they would include in terms of personal property or furniture? this one made me laugh. pretty please, could they leave behind the ugly dorm light and random bookshelf in the bedroom?

- Purchase Price – keeping this under wraps for obvious reasons

- Contract Deposit – 10% of total purchase price (YIKES) (Due at the time the Contract is signed by you)

- Closing Date – On or about May 2, 2016 (this changed)

- Maintenance –keeping this under wraps for obvious reasons

- Assessment – None.

- Loan Amount – keeping this under wraps for obvious reasons

- Occupants – Sarah Jacobson

- Pets – None. this had to be corrected to include the queen of my life, my cat, penny lane

- Seller’s Rider 42 – Please Review and confirm that all is true.

- Appliances – Seller is not making any representation that any of the appliances are in working order. Are you replacing them all anyway? this also made me laugh. i kid you not, i asked my lawyer to write “please remove the fridge” into the rider to ensure that whatever dead body is hiding inside there will NOT be in my apartment when the keys are turned over to me.

following this list, my lawyer had another one. this one was made up of “everything he could find out about the Corporation (apparently, that’s what the co-op is called) and the building.”

and in that list was this SNEAKY LITTLE ITEM:

Flip Tax – 25% of the net of any first sale of a unit and after the first sale its 15% of the net sale price or $5,000.00, whichever is greater.

i’m sorry, SAY WHAT? i read it multiple times, then read it again. after i handed over all of my savings, a good chunk of my inheritance, my first born, an exhaustive list of my financials and also my soul, THE CO-OP WAS GOING TO TAKE 25% OF THE APARTMENT WHEN I SOLD IT?

oh HELL no.

i called my broker. he told me he’d mentioned this to me, that flip tax was a common thing in the new york real estate world.

look: i know i tend to have selective memory. that and i smoked too much weed in college and so sometimes my memory just isn’t that great. but i swear to god, NO ONE had mentioned this tax. and CERTAINLY, no one had mentioned it in the context of my making an offer on the grand apartment.

my broker tried again. he explained that while i had correctly understood the concept of flip tax, i hadn’t interpreted the ruling above quite right. the “first sale,” he told me, refers to, well, just that. as in, the first people to sell the apartment following its conversion from a rental unit to a co-op unit would pay 25% of the profit. basically, it works like this:

seller A: the lucky person who was living in the unit when the building went co-op in the 1980s. likely got the apartment for a steal (seriously, i don’t even want to know what they paid, it’ll make me cry), and then made a BOATLOAD of money the first time they sold it. let’s just say, for shits and giggles, they bought the apartment for 80k.

seller A’s flip tax situation went a little something like this:

purchase price: 80,000

selling price (the first time the apartment was sold by seller A, the original owner): 500,000

profit made on the unit = 500,000 (selling price) – 80,000 (purchase price) = 420,000

flip tax = 420,000 x .25 = 105,000.

INSANITY, RIGHT? basically, seller A had to hand over 100 grand of their profit to the co-op. you know, because life makes no sense.

i thought this was the situation i was in.

while i wasn’t exactly right, i wasn’t exactly wrong, either. because the “first sale” already happened, my piece of the pie is “only” 15%, not 25%. that softened the blow, a little bit. and that 15% only applies, remember, to the profit i make – not to the gross selling price.

a little research, along with more discussion with my broker, revealed that flip taxes are pretty standard in new york city co-ops. they allow the co-op to make money without having to jack up the maintenance (which, i should add, is quite low in this building).

in other words, as frustrating as that 15% is, there’s no way around it. though it may not be the LOWEST in all the land, it’s also not the worst case scenario (that would be a flip tax percentage that applies to the gross selling price. OUCH).

all parties involved in the transaction (broker, lawyer, mortgage broker, and a few other smart people i talked to) agreed that while 15% wasn’t, you know, great, it also wasn’t the end of the world, nor was it a reason to walk away.

so, i signed. but may this be a lesson for all future apartment hunters: ask about the flip tax, and ask about it early. preferably before you fall in love with a future home and imagine raising your little four legged friends (and maybe even some two legged ones) there.

hindsight’s 20/20, right?

above: my friends sara and martha, who i took to see the grand apartment over memorial day weekend. i thought i would close a few days afterwards.

above: my friends sara and martha, who i took to see the grand apartment over memorial day weekend. i thought i would close a few days afterwards.